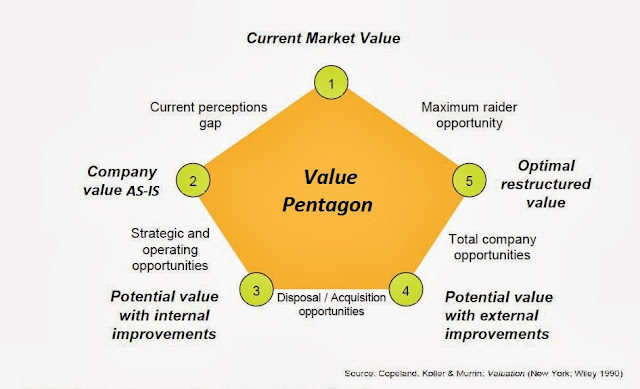

Value Pentagon

Company as-is value is the value of the company without any restructuring or change.

The company’s optimum value is the value that can be achieved after the restructuring is done.

Internal restructuring: Find out redenancies, wastages, remove bottlenecks.

External Restructuring: Merger, demerger, acquisition, etc.

Financial restructuring: Writing down useless assets, debt restructuring etc.

Shareholder vs Stakeholder value

When we talk about the value of the company, they normally have two approaches, increase shareholder value or stakeholder value. Both approaches have their pros and cons. The shareholder value approach is easy to track, as you can look at the numbers and figure out if the shareholder value has increased. But at the same time, this approach can be myopic and focus on short-term goals.

The stakeholder value approach has a broader view, where it talks about customers, employees, society, shareholders, and other stakeholders. The problem here it is hard to track as there is no direct way to track it. For example, giving better discounts and better salaries might help me keep my customers and employees happy, but might add to losses.

Measuring shareholder wealth creation

Market Value Addition or MVA is an important aspect to understand shareholder value. For example, there are two companies, A and B, both with a market cap of say 1000 crore. But the network of company A is 500 crore and company B is 250 crore. We can see MVA for company A is 500 crore whereas company B is 250 crores. In other words, the market view potential for growth in company B.

Corporate Restructuring

Corporate restructuring includes acquisitions, demergers, joint ventures, etc. For example, buying Corus helped Tata steel to jump from 55th ranked in steel revenue worldwide to 5th rank.

Corprate restructuring can be done by

Expansion: Absorption, Tender Offer, Asset acquisition, Joint venture, etc.

Contraction: Demerger – Spin off, split off, split up, Equity carve out etc.

Corporate Control: Going private, Equity buyback, leveraged buyout, etc.

Corporates can unlock value by demergers. Studies report that the observed value of the diversified firm is, on average, 15 percent less than the sum of the implied market value of its divisions, as compared to stand-alone market values of single-segment firms in those industries.

Factors behind diversification discount

Information hypothesis: the inability of markets to correctly evaluate conglomerate structures with unrelated businesses, leading to possible undervaluation.

Inefficient Management hypothesis: the inability of the managers to efficiently manage unrelated businesses.

Inefficient investment hypothesis: distortion of investment due to competition among units for resources.

Modes of asset disposition

Slump sale: Slump sale means the transfer of one or more undertakings as a result of the sale for a lump sum consideration. For example, Ruchi Soya buying biscuit business from Patanjali Natural Biscuits Pvt Ltd (PNBPL) for 60 crores.

Spin-Off: A spinoff is the creation of an independent company through the sale or distribution of new shares of an existing business or division of a parent company. When a new company B is carved out of company A, mostly shareholders of company A will get some proportional shares of company B.

Spin-Off helps in

- Unlocking hidden value: establish a public market valuation for undervalued assets.

- Undiversification: divest non-core business and sharpen strategic focus

- Institutional sponsorship: Promote equity research coverage

- Public currency: the public currency for acquisition and stock-based compensation programs

- Motivating Management

- Eliminating dis-synergies

- Corporate Defence: Divest “crown jewel” asset to make the takeover of parent company less attractive.

Challenges in spin-off: There are certain aspects that need to be managed, for example, if the parent company has debt, how this debt will be divided between parent and spin-off company. The lenders need to agree on the arrangement.

Split-Off: In a split-off, the parent company offers its shareholders the opportunity to exchange their parent-co shares. For example, a big shareholder can give up shares in the parent company to gain controlling stakes in the new company.

Split-up: Division of a company into two or more publically traded companies. The difference here is that instead of the parent company and spun-off company, we have completely new companies into existence.

Equity Carve-out: Also known as IPO carve-out, the parent company sells a portion or all of its interests in a subsidiary to the public in an initial public offering.

Financial Restructuring

Cleaning up a balance sheet: writing off losses, writing down useless assets, can be done through asset restructuring and recapitalization.

Debt Restructuring

- Strategy-Driven: Restructure debt by lowering the interest rates.

- Crisis-Driven: When a company defaults, the company is forced to restructure debt.

Equity Restructuring

- Special dividend: One-time dividend

- Share buyback: reduces the shareholder base. As a regulatory requirement, the debt-equity ratio should be 2:1, after the buyback. Buyback can happen through the open markets, tender offers, and buyback from employees.

- Stock Splits: helps with liquidity

- Bonus Shares: When the company is growing fast but does not want to distribute cash in form of a dividend, a bonus share will help reward the shareholders.